An Essential Guide to Accounts Payable Fraud

This guide outlines the types of accounts payable fraud, red flags and strategies for detecting, preventing and investigating accounts payable fraud.

Accounts payable fraud, also known as AP fraud, is among the most ubiquitous and damaging of frauds that affect businesses of all sizes. It's also among the easiest frauds to perpetrate, since most of the money leaving a company legitimately goes through the accounts payable function. The ACFE's Global Fraud Study identified three types of accounts payable (AP) fraud - check tampering, billing schemes and fraudulent expense reimbursements - as accounting for the largest percentage of reported fraud cases. Check tampering alone results in a median loss of $158,000 per business. But there are many schemes and new ones emerging as fraudsters figure out ways to skirt fraud controls in new ways.

Protect Your Company from AP Fraud

Looking to keep your company safe from the damages of accounts payable fraud? Download this free cheat sheet for eight easy anti-fraud controls you can implement right now. Download Cheat Sheet

Red Flags for Accounts Payable Fraud

Most AP fraud schemes involve an employee hiding fraudulent transactions among thousands of legitimate transactions. Finding them can be like looking for a needle in a haystack, unless you know what to look for. Many of the red flags for accounts payable fraud are the same as red flags for any type of fraud. For example, if you notice employees living beyond their means, not taking vacations, engaging in reckless behavior, withholding information or staying late and coming in on weekends, it's wise to investigate further. Suspect accounts payable fraud? Download our free cheat sheet: 16 Ways to Identify Suspicious Vendors. But there are also some indicators that are specific to the accounts payable department, and every anti-fraud programs should include regular audits that screen for these "needles in a haystack" as well as the more general red flags.

Look for these AP fraud red flags:

- Vendors that seem unusual or are unapproved

- Increases in payments to particular vendors without corresponding increases in goods or services

- Very large payments to one vendor

- Unusually large purchases on an employee's company-issued credit card

- Payments that consistently fall just under the amount requiring authorization

- Invoices in sequence

- Invoices that look unprofessional or photocopied

- Invoices that are missing key details, such as address and phone number

- A vendor's email address that uses a free provider, such as Gmail

- Multiple invoices paid together or on the same date

- Vendor addresses that are the same as an employee address

- Vendor address that look to be residential addresses

- Vendors with similar names

- Large entertainment and gift charges

- Rounded dollar amounts

- Incomplete documentation or copies instead of originals

- Duplicate payments to the same vendor

- Vendor's prices that seem unusually low or high

- Close relationships between an employee and vendor

- Repeated purchases from a vendor with a record of poor quality goods or services

- Tips or complaints from employees, customers or vendors

Types of Accounts Payable Fraud

Billing Schemes

In its most general form, a billing scheme involves employees generating false payments that are eventually (or immediately) paid to themselves. There are many ways employees can do this.

- Creating false invoices for products or services that were not delivered.

- Colluding with a third party, passing invoices through an account or company the employee controls and taking a cut of the payment in what's known as a "pass-through scheme"

- Initiating purchase orders and payments for goods or services for personal use.

- Setting up a fake vendor account and creating false invoices which are paid to the employee.

- Processing duplicate payments to a vendor, and when the duplicate is returned from the vendor, the employee keeps it. Or processing duplicate payments to create a credit with the vendor then keeping the vendor's next payment.

The 2017 Hiscox Embezzlement Study found that two billing schemes, vendor invoicing and false billing, accounted for just 14 per cent of the cases examined but incurred 42 per cent of the dollar losses. These cases involved employees fabricating or inflating vendor invoices or creating fictitious vendors. The study also found that check fraud was used in 22.1 per cent of cases, more than half of which were committed by managers.

Check Fraud

Check tampering, or check fraud, is among the most lucrative of the accounts payable fraud schemes. Done well, this fraud can be hard to catch. Done badly, the paper trial created by check fraud is easy for an investigator to follow and easy to prosecute because of the documentation it creates.

ACH Fraud

ACH fraud, or automated clearing house fraud, is becoming more common, especially with same-day turnaround on ACH transactions. One way to commit this fraud is for employees in the accounts payable department to set themselves up as automatic bill payees in the system. An employee might set up a new payee and send funds, or even divert funds to a new account using an existing payee account but changing the details.

Expense Reimbursement Fraud

Expense reimbursement fraud can be committed by any employee has business-related expenses that are reimbursable and, according to the ACFE, this type of fraud lasts an average of two years before being detected. Expense reimbursement fraud is usually achieved through one of the following:

- Mischaracterized expenses

- Overstated expenses

- Fictitious expenses

- Double claims

Kickback Schemes

Kickback schemes, also known as corporate bribery, take place when a vendor pays an employee of a company (buyer) to purchase - or influence the purchase of - products or services offered by the vendor. Sometimes kickbacks are in the form of cash, which is difficult to trace. But kickbacks can also be entertainment, travel, gifts, use of the vendor's goods or services, promises of employment for the employee or his/her family or friends, etc.

Conflicts of Interest

A conflict of interest occurs when an employee has a vested interest in a company that does business with the employee's company. This doesn't constitute fraud in itself, but it does create a situation that is ripe for fraud. An employee in the accounts payable department with an undisclosed conflict of interest is in a position to overpay, collude with or provide unfair advantages to a vendor with which he or she has a relationship.

Conducting an AP Fraud Investigation?

You'll need the right tools. This Investigation Plan template will guide you along as you investigate. Download our Investigation Plan Template

Investigating AP Fraud

A forensic accountant can be helpful for investigating AP fraud, but you don't always need to bring in experts, especially in the preliminary stages. Start by interviewing any witnesses, managers and co-workers of the accused person, as well as human resources personnel who may have information related to the case. Outside the company, interview vendors, customers and employees of vendors who also many have information about the fraud. You may also get valuable information from competitors, agents, distributors, or anyone else who may have insight into, benefitted from or suffered as a result of the fraud.

Look for Evidence

Examine any documents that could be relevant, including:

- Checks

- Invoices

- Vendor contracts

- Pricing documents

- Journal entries

- Bank statements

- Check deposit registers

- Payments registers

- Vendor files

Preventing and Detecting AP Fraud

According to the ACFE's Report to the Nations, victim organization that lack anti-fraud controls suffer double the median losses of those with anti-fraud controls in place. So it's critical that every accounts payable department have robust fraud controls in place.

Verify Vendors

Establish mechanisms for approval of all new vendors added to the company's vendor files. This should be done by someone separate from the person who adds new vendors. Conduct regular vendor audits to verify that all vendors are legitimate. Look for the red flags listed above and manually verify, by telephone, online or in-person, any questionable ones.

Reconcile Accounts

Match accounts payable entries with the company checkbook each month.

Review Transactions

Examine transactions to look for indicators of fraud. Check for the red flags listed above, such as round numbers, gaps in invoice numbers, unusual transactions, unusual frequencies or amounts.

Implement a Check Review Procedure

This procedure should be conducted by someone who isn't involved in check issuing, and occur before checks are distributed. Implement a two-signature requirement for checks above a certain amount and scan the register for checks that fall just under this threshold.

Conduct Unscheduled Audits

Perform random audits of accounts payable files to check for all red flags listed above.

Rotate Employees Through the AP Function

This will require cross-training, but will reduce the likelihood of employees conducting long-term AP fraud schemes or nurturing relationships with vendors.

Implement Mandatory Vacations

Implement mandatory vacations for employees in the accounts payable department to increase the likelihood of long-term schemes being uncovered. Detect and prevent fraud more effectively and quickly with a fraud response plan. Use our template to get started.

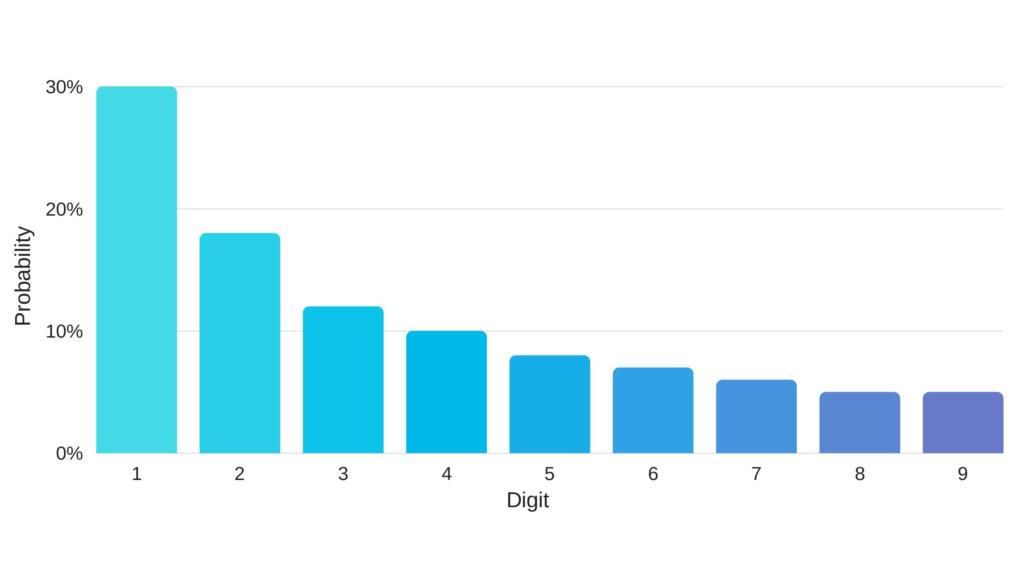

Uncover AP Fraud with Benford's Law

Benford's Law is a great mathematical tool for screening accounts payable records for fraudulent payments. Benford's Law outlines a pattern of naturally occurring numbers that should be consistent across any set of "natural" numbers, such as payment records. When numbers are manually added into a naturally occurring set of numbers, they don't match the pattern dictated by Benford's Law. Discovered by Frank Benford, an American astronomer, in 1881, Benford's Law states that the expected occurrence for 1 as the first digit in a natural number is 30.1 per cent. The numeral 2 is expected to be the first digit 17.6 per cent of the time and the numeral 3 should be the first digit 12.5 per cent of the time. The pattern continues through to the numeral 9, which should be the first digit in a natural number 4.6 per cent of the time.

If a company has a rule that expenditures over a certain amount, say $1,000, require a second signature, an accounts payable employee writing fraudulent checks might keep the amounts below that threshold. In this case, a disproportionate number of checks might be written for amounts in the 900s, with a starting numeral of 9. Since the numeral 9 should occur naturally as the first digit only 4.6 per cent of the time, a lot of payments beginning with a 9 will throw the number set off the expected pattern. This is a red flag in an audit of accounts payable records. There may, of course, be a logical explanation for numbers not falling in line with Benford's Law, but it is an indicator that something is influencing the numbers and breaking the natural pattern. The fraud examiner then can investigate the cause of the anomaly to see if there is fraud occurring.

Combating Expense Fraud in Particular?

Expense fraud can run rampant in workplaces. This cheat sheet outlines ten basic strategies you can put implement today to prevent expense fraud in your organization. Download Cheat Sheet

Company Culture and Fraud Prevention

One of the best, most positive, ways to reduce accounts payable fraud is to nurture happy employees and a company culture that discourages dishonesty and encourages open communication. Having a company ethics hotline and a robust system for collecting and investigating employee complaints and tips will go a long way in preventing and detecting accounts payable fraud.

Ready to Transform Your Investigation Process?

Join 80,000+ professionals who trust Case IQ to streamline their case management and ensure compliance.